Uber’s 2023 numbers are staggering: 150 million “Monthly Active Platform Consumers”. Gross bookings $138 billion. Adjusted-EBITDA $4.1 billion. GAAP Income from Operations $1.1 billion. 70+ countries, 10,000 cities. 6.8 million drivers & couriers. Profitable. Uber is undoubtedly THE #1 mobility player, but the company also faces some challenges. Let’s dig in.

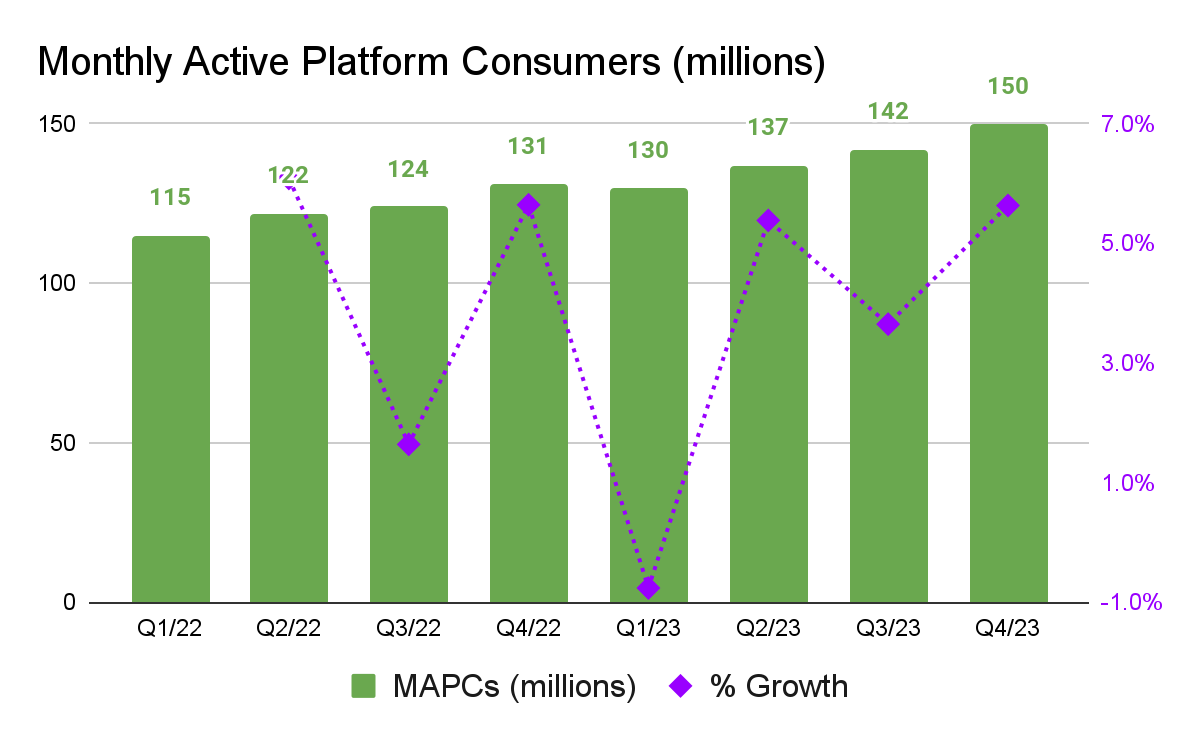

From the beginning of 2022 to the end of 2023, “Monthly Active Platform Consumers” (MAPCs) grew 13.6% year-on-year (YoY), to 150 million in Q4/2023.

From the beginning of 2022 to the end of 2023, “Monthly Active Platform Consumers” (MAPCs) grew 13.6% year-on-year (YoY), to 150 million in Q4/2023.

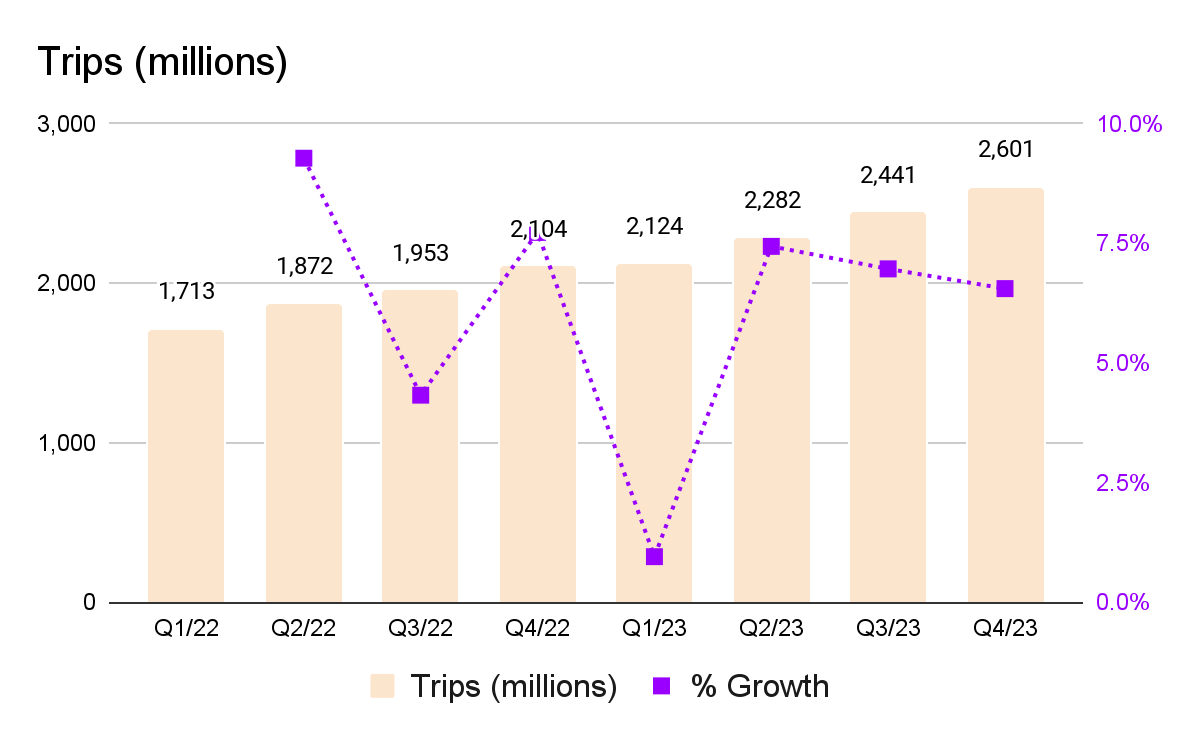

Trips grew at a faster rate, 23.6% YoY, to 2.6 billion. In (a very simple & indicative) average, Uber’s consumers are taking more trips per year, from 14.9 in Q1/22 to 17.3 in Q4/23.

Show me the money. Gross bookings in 2023 were $137.8 billion, up 19.5% YoY. Mobility leads growth, with freight falling behind with negative growth numbers.

| 2022 | 2023 | % change YoY | |

|---|---|---|---|

| Mobility | 52,665 | 68,897 | 30.8% |

| Delivery | 55,778 | 63,726 | 14.2% |

| Freight | 6,952 | 5,242 | -24.6% |

| Gross Bookings | 115,395 | $137,865 million | 19.5% |

And the way this table looks on a graph, split into quarters:

Coming out of the pandemic, it was deliveries that brought in more $ order volume in, now Mobility has taken the lead, with 50% of total gross bookings vs. Delivery’s 46.2%.

“In 2023, we generated 15% of our Mobility Gross Bookings from trips that either started or were completed at an airport.”

Uber Investor Update 2023

That figure amounts to $10.3 billion gross bookings, from airport activity alone.

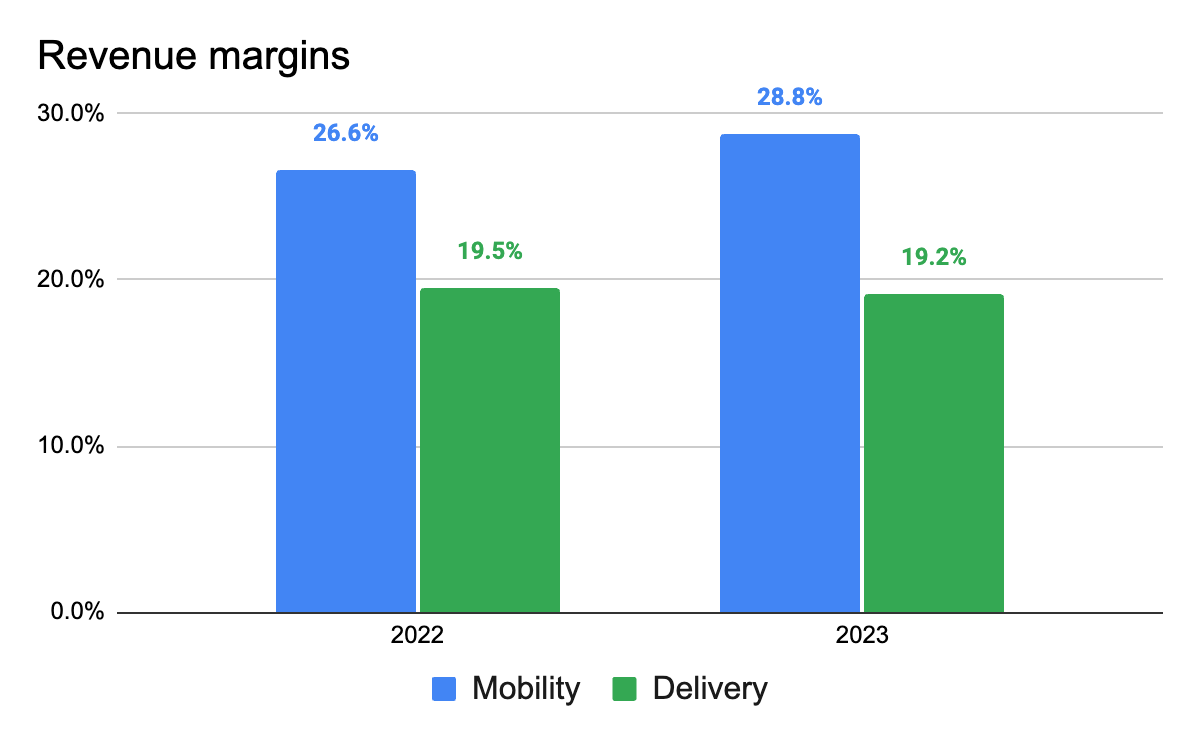

On our way to understand Uber’s finances, let’s talk margins. In 2023, Mobility margins rose to 28.8%, Delivery with a bit of decline to 19.2%. In total, Uber makes 27% margin (revenue/gross bookings).

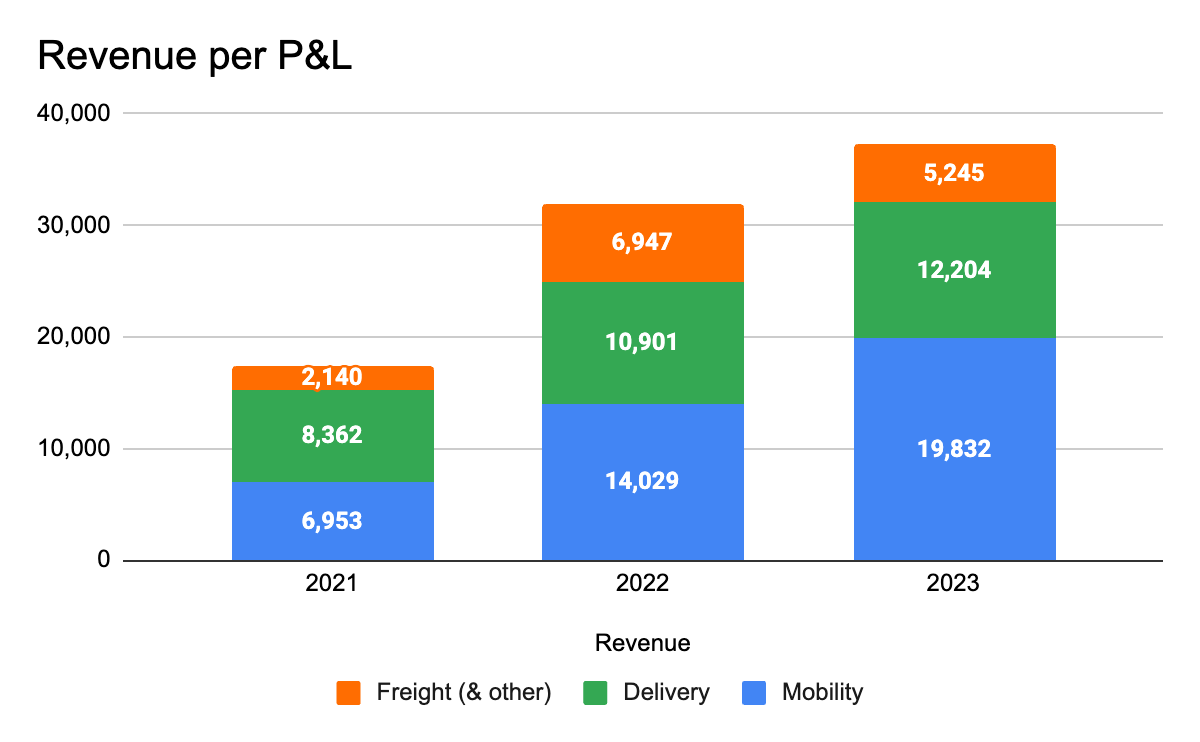

Which leads us to explore profitability at Uber’s three divisions: in 2023 Mobility makes up for 53.2% of Uber’s revenue; Delivery 32.7% and Freight & other 14.1%. Total revenue growth was 17%.

| 2021 | 2022 | 2023 | % change 22-23 | % of total 2023 | |

|---|---|---|---|---|---|

| Mobility | 6,953 | 14,029 | 19,832 | 41.4% | 53.2% |

| Delivery | 8,362 | 10,901 | 12,204 | 12.0% | 32.7% |

| Freight (& other) | 2,140 | 6,947 | 5,245 | -24.5% | 14.1% |

| Revenue | 17,455 | 31,877 | $37,281 million | 17.0% | 100.0% |

“In 2023, we derived 20% of our Mobility Gross Bookings from five metropolitan areas—Chicago, Los Angeles, and New York City in the United States, Sao Paulo in Brazil, and London in the United Kingdom”.

Uber Investor Update 2023

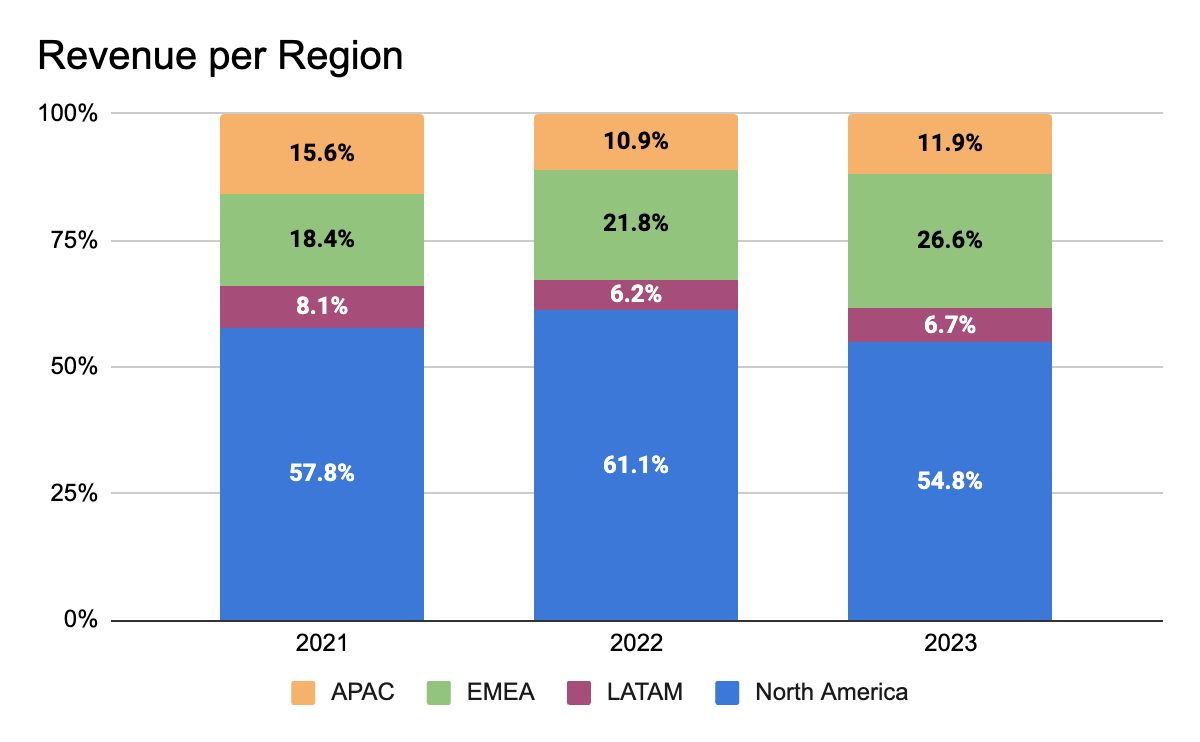

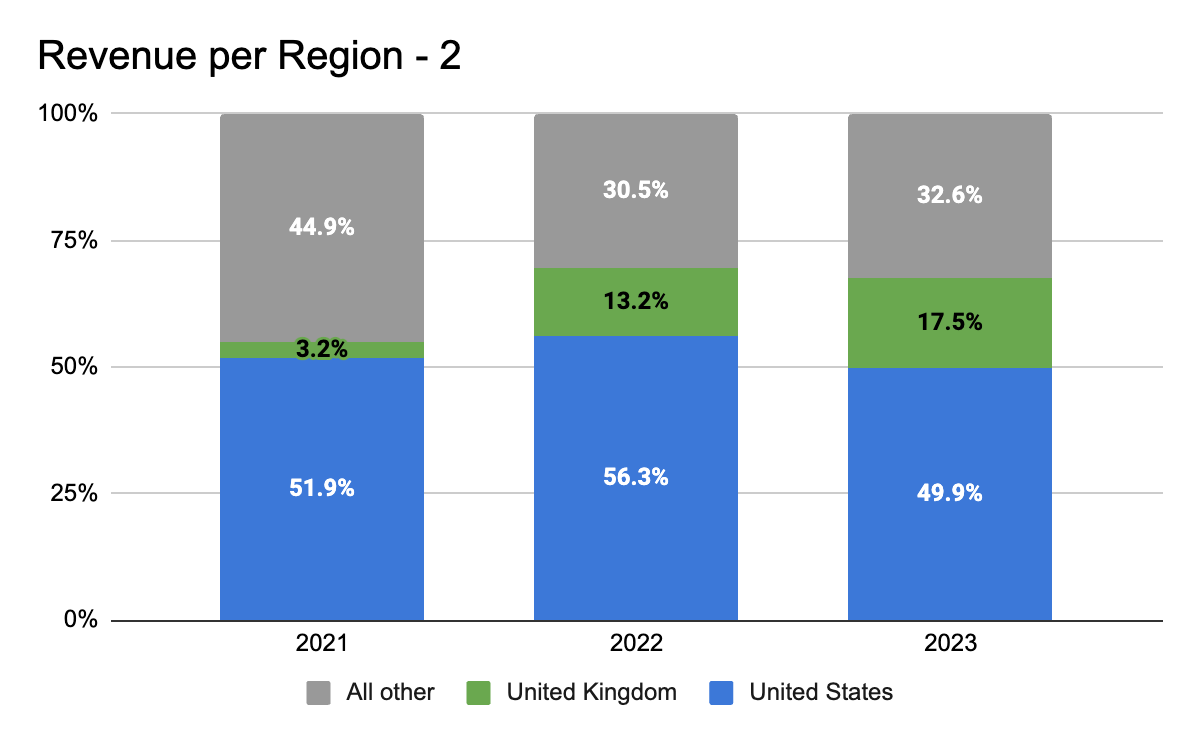

Uber has an opportunity and a challenge – its revenues are concentrated on the US and the UK – in 2023, 67.4% of revenue came from those two countries!, with the US alone accounting for 50% of Uber’s total revenue.

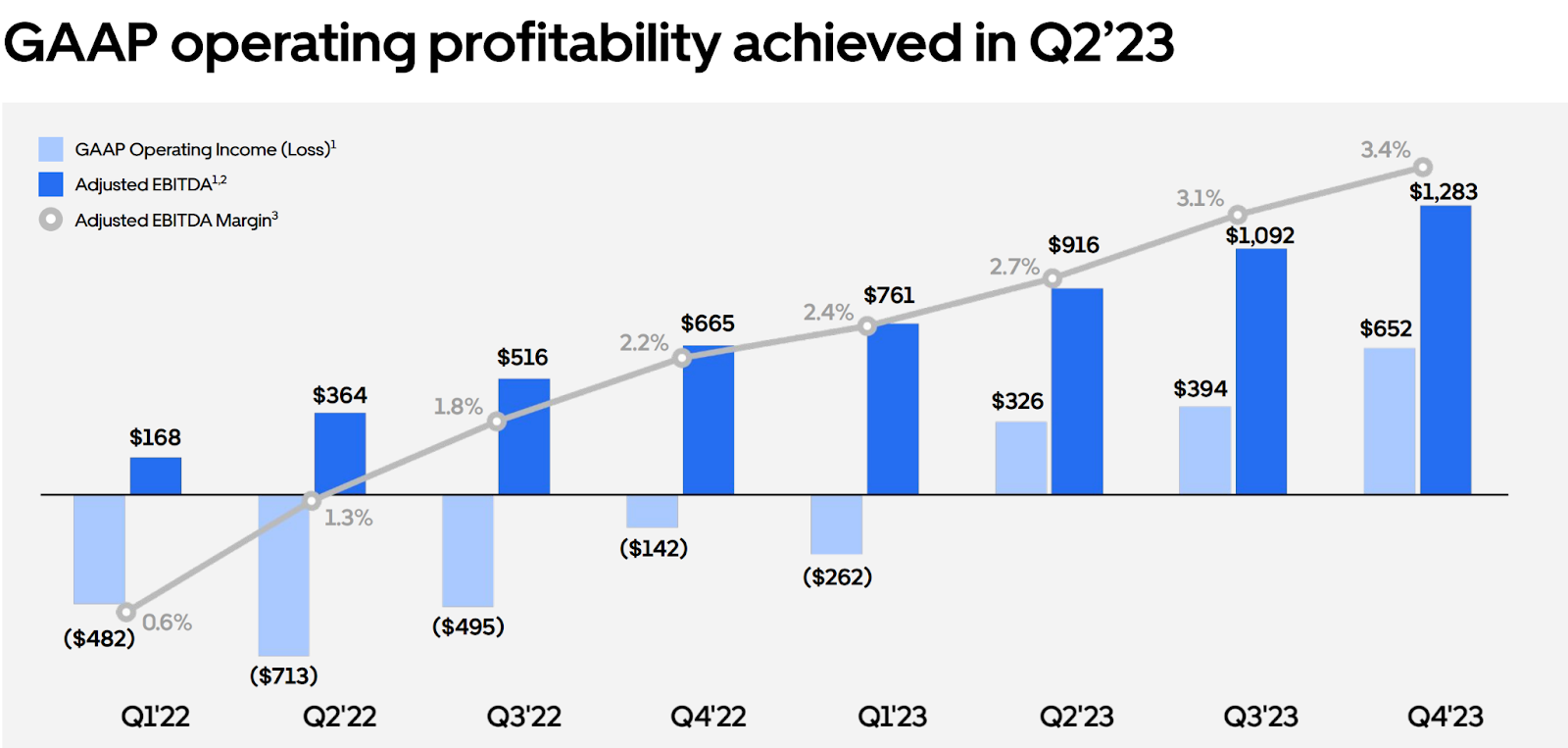

Now to profitability – Adjusted-EBITDA profitability was achieved in Q1/22, and GAAP operating income profitability in Q2/23, leading to full year GAAP profitability.

Uber’s profitability is thin – in 2023 Income from operations was 2.98% of revenue; net income (the most bottom line) was 5.06%, the 2% difference is mostly attributed to gains from income from non-controlling interests (i.e. holding in other companies).

In 2023, Uber attributed $5 billion Adjusted-EBITDA to Mobility, and $1.5 billion to Delivery.

Uber Investor Update 2023

To achieve profitability – Uber mostly reduced expenses in “Sales & Marketing” and in “General and Administrative”.

Uber’s focus for the coming years

Mobility

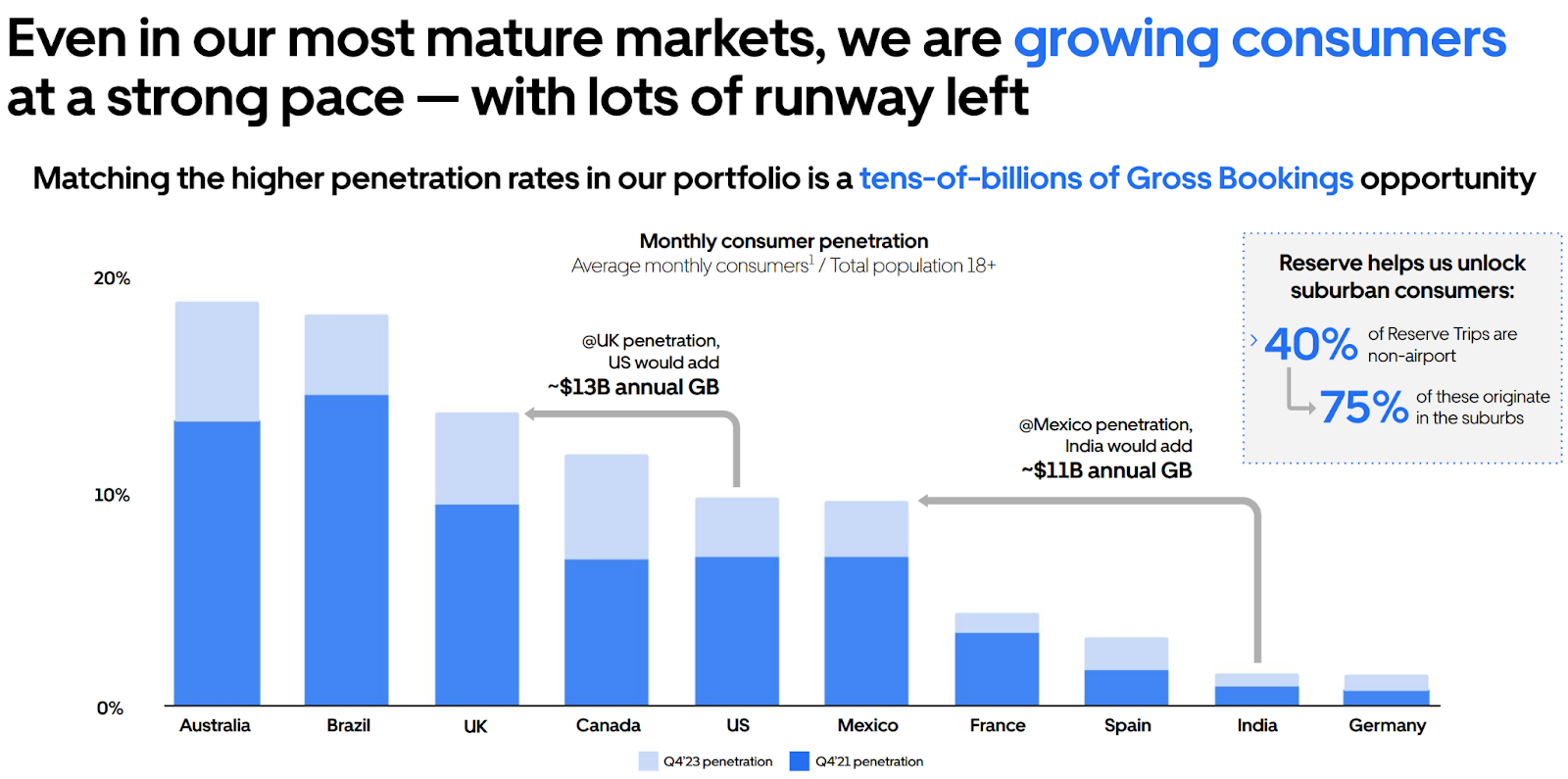

Uber sees itself competing against the private car, hence has plenty room to grow. Per Uber, “Reserve” (pre-book) opened up suburban opportunities; the company expects growth in Airport solutions, Uber for Business, Uber Health, Advertising and the Teens solution; plans to grow the breadth of mobility services, from rickshaw & shuttles to Black & SUV, with a focus on lower cost solutions; and targets growing the number of average rides.

Uber Investor Update 2023

Drivers

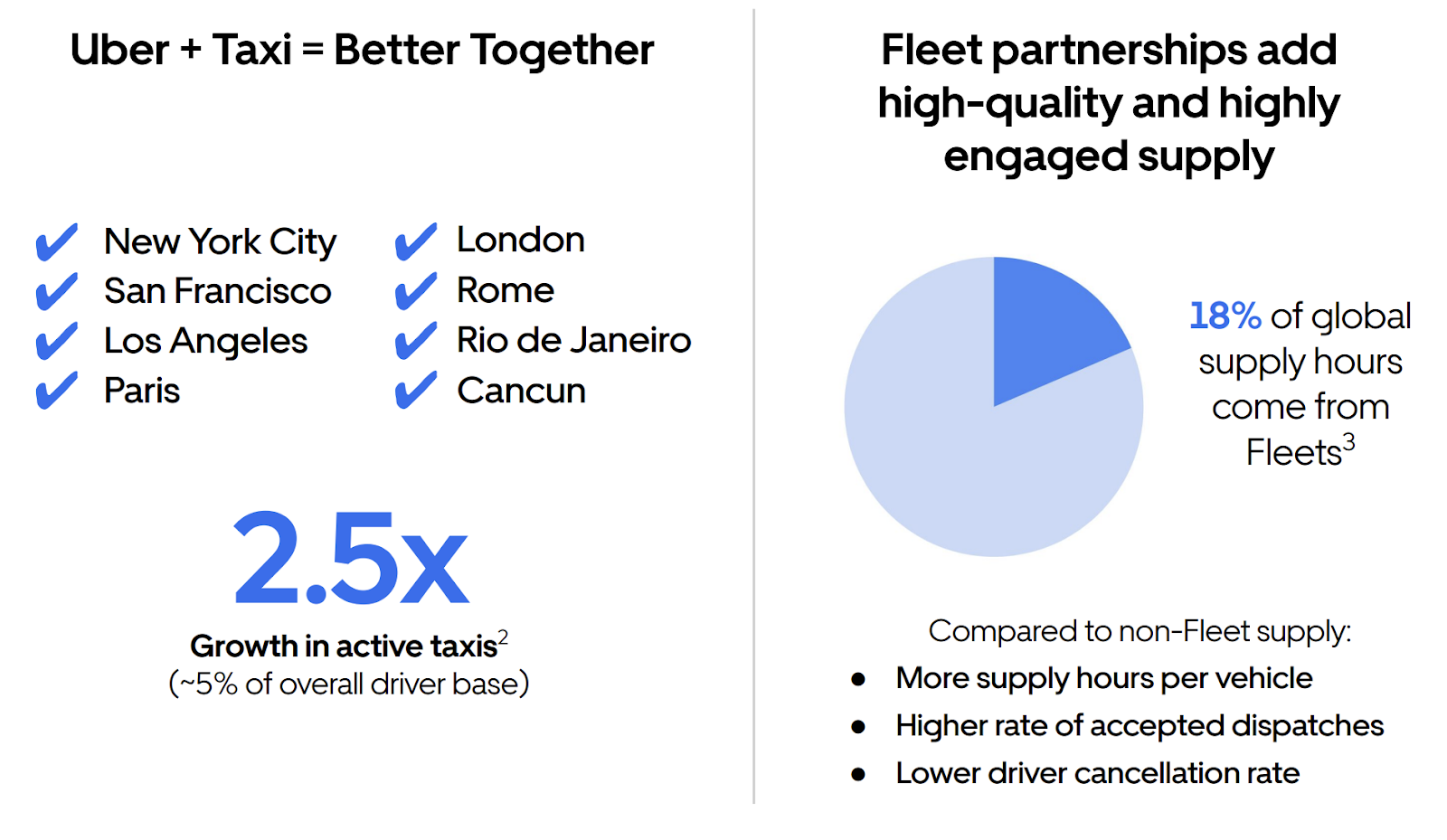

Uber has 235,000 taxi drivers in 33 countries, with 5% of Uber’s rides supplied by taxi. The company is committed to increase that number by partnering with taxis and professional fleets, which are 18% of Uber’s supply today. I wrote about this in the past, as this is a good way to ensure supply with a lower cost-of-acquisition.

Uber Investor Update 2023

Delivery

Delivery is still a growing product for Uber, in 2023 growing 12% in revenue YoY. Uber’s focus is on lowering operational costs and promotions to achieve higher probability; cross-selling; adding grocery (which is very different to food); creating more partnership and growing the advertising product and revenues.

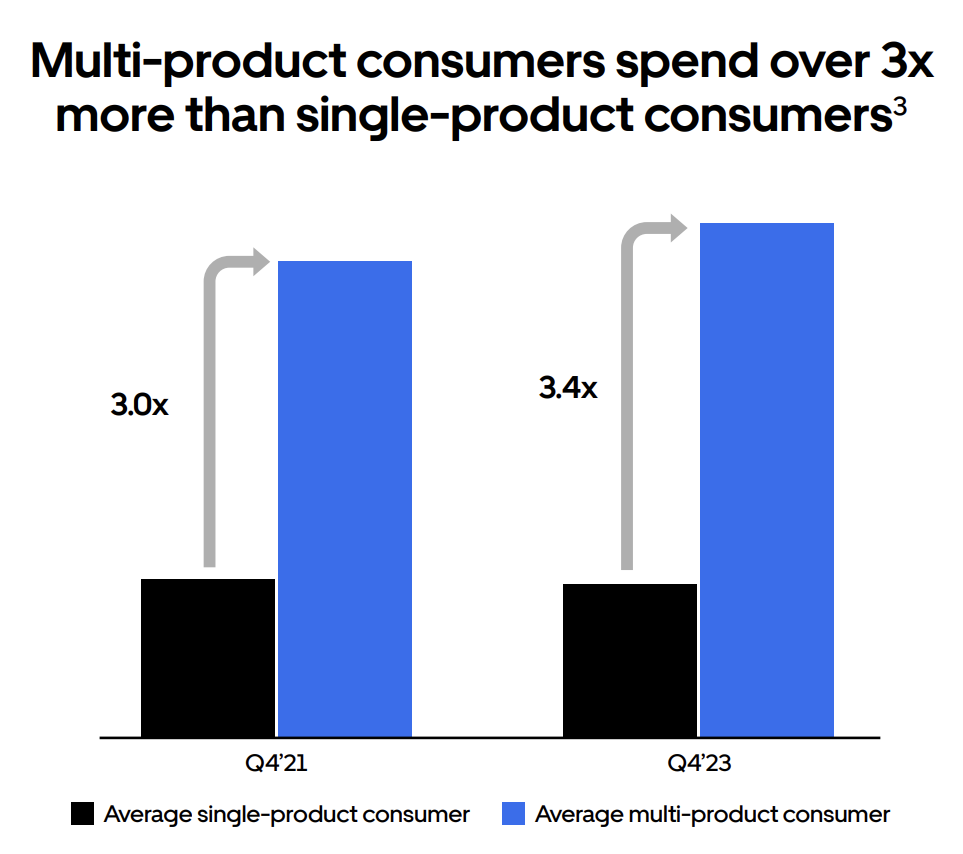

Multi-product (mobility & delivery)

Consumers who use BOTH mobility and delivery services – 34% of Uber’s consumers – are likely to spend X3.4 on the Uber platform than those who use either mobility OR delivery. It makes sense that increased usage is brought by increased loyalty, and therefore leads to increased spend. As cross-platform acquisition costs are as much as 50% lower, it is clear that Uber’s goal is to encourage multi-product(ness).

Advertisement

Uber Investor Update 2023

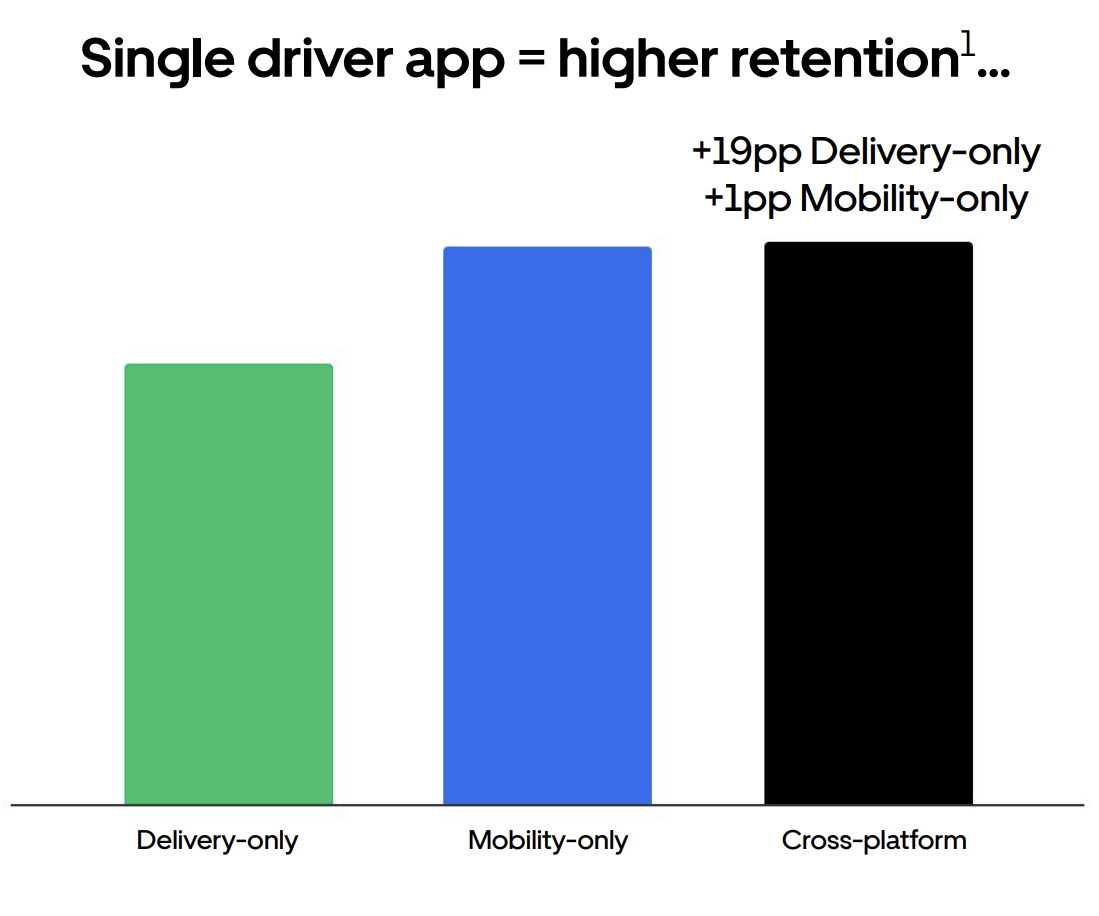

For drivers, multi-product leads to higher retention & engagement and lower cost of driver acquisition. Data also indicates that drivers who perform mobility rides only are less encouraged to cross-platform, which could explain why Lyft has been advocating a delivery-less platform for its drivers.

Multi-product leads us to Uber One membership subscription

Uber is growing Uber One. The service has 19 million members – 12.7% of all Q4 monthly active consumers. On one hand, it drives engagement, with users spending X3.4 more on the platform; on the other, profitability from those users is lower, as the program really does deliver benefits for the consumer.

This number, X3.4, is the same number attributed to multi-product usage, which makes one wonder about the overlap here.

Uber’s challenges

Five challenges that came out from reading the report:

- Profitability margins – Uber’s “Income from Operations” is 3%. Any change for the worst, such as s new driver shortage, could jeopardise profits.

- Freight – Uber doesn’t have this solution figured out yet; YoY gross bookings fell 24.6% and revenue 24.5%.

- Room for growth? – Uber speaks about competing against the private car and having much room to grow in, both from existing and new users. After 15 years of operations, is that really true, or is Uber’s total addressable market (TAM) more limited than the company hopes it to be?

- Gig-economy employment status – around the world politicians are getting closer to the point of needing to decide on whether these workers are employees or independent contractors. It is not only a matter of politicians trying to score points with voters or trying to secure corporate donations, but a real social-security and pension bomb that is going to explode in years to come. How that legislation will be formed will greatly affect Uber’s top and bottom line.

- Dependence on US & UK revenues – the former constituting 50% of total revenues, The latter 17.4% – together 67.4%. While Uber can expand operations elsewhere, it also faces fiercer competition in those regions. The chances of massively losing market share in the US & the UK are small, still that is a possibility Uber should be mindful of.